What Is a Basis Point? Basis Points Explained + Easy BPS to Percentage Converter

Imagine the Federal Reserve announces it's hiking interest rates by 25 basis points. Headlines scream, markets jitter, and your portfolio feels the ripple. But what does that actually mean for your savings account, mortgage, or investments? Is it a quarter of a percent? Half? The ambiguity vanishes once you grasp basis points—one of finance's simplest yet most powerful tools. In this guide, we'll demystify what is a basis point, why it matters, and how to convert basis points to percentage effortlessly. Whether you're tracking Fed moves or decoding ETF fees, you'll walk away equipped.

What Is a Basis Point? A Crystal-Clear Definition

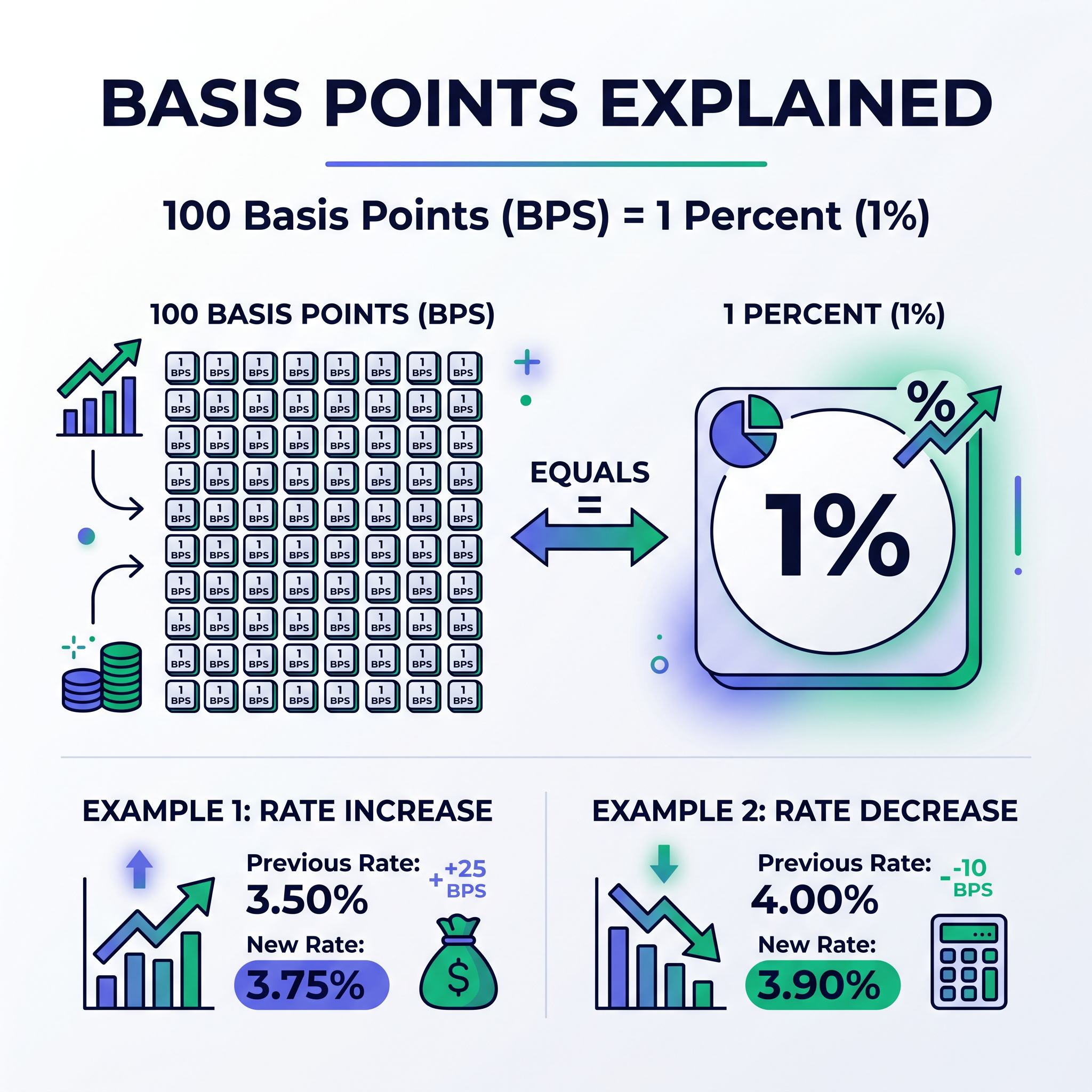

Basis points explained starts with precision: one basis point (often abbreviated as bps, pronounced "beeps") equals 0.01%, or one-hundredth of a single percentage point. Think of it as slicing a percentage into 100 tiny pieces. A full percentage point? That's 100 basis points. No more fumbling with decimals that trip up even seasoned investors.

Picture a seesaw: percentages swing broadly, but basis points offer the fine-tuned balance. Born in the trading pits of Wall Street, this unit eliminates confusion in high-stakes conversations where 0.01% can mean millions. Central bankers, bond traders, and mortgage lenders all speak this language fluently.

Why Basis Points Matter: Cutting Through the Ambiguity

Why bother with bps when percentages seem intuitive? Ambiguity. Say rates rise "0.50%"—is that a 0.50 percentage point jump (like from 5% to 5.50%), or a relative 0.50% increase (from 5% to 5.025%)? The former is clear in basis points: 50 bps. The latter? A murky 25 bps on a 5% base. Basis points standardize everything as absolute moves, sidestepping relative math that muddies waters.

In volatile times—like the Fed's post-pandemic rate blitz—this clarity is gold. A 25 bps hike might nudge your credit card APR just enough to rethink that balance, or shave yield from bonds you're holding. Investors ignore it at their peril; students, embrace it for decoding textbooks and news alike.

Basis Points to Percentage: Formulas and Fast Conversions

The Simple Formulas

Converting basis points to percentage (or vice versa) is child's play. Here's the step-by-step:

- BPS to Percentage: Divide by 100. Example: 50 bps ÷ 100 = 0.50%.

- Percentage to BPS: Multiply by 100. Example: 0.75% × 100 = 75 bps.

That's it—no calculators needed for basics. But for quick reference, bookmark this handy table covering 1 bps to 1000 bps.

| Basis Points (bps) | Percentage (%) |

|---|---|

| 1 | 0.01% |

| 10 | 0.10% |

| 25 | 0.25% |

| 50 | 0.50% |

| 100 | 1.00% |

| 250 | 2.50% |

| 500 | 5.00% |

| 1000 | 10.00% |

Pro tip: For our BPS to percentage converter, head to our free tool below—no math required.

Basis Points in the Real World: Key Financial Contexts

Basis points aren't abstract—they pulse through markets daily. Here's where they shine.

Central Bank Rates

The Fed's 25 bps hike? That's the federal funds rate ticking up 0.25%, rippling to everything from auto loans to stock valuations. Track announcements: a 50 bps cut signals recession fears, boosting bonds.

Bond Yields

Treasury yields widen or tighten in bps. A 10-year note yield jumping 15 bps means higher borrowing costs economy-wide, pressuring growth stocks.

Mortgages and Loans

Your 30-year fixed jumps 37 bps? That's ~$100 more monthly on a $300K loan. Shoppers watch spreads: mortgage rates often trail Treasuries by 150-200 bps.

ETF and Fund Expense Ratios

Low-cost ETFs boast 3-10 bps fees. Vanguard's VTI at 3 bps? Versus 100 bps for active funds, that's thousands saved yearly on a million-dollar portfolio.

Credit Cards and Spreads

Cards charge prime + 15-25% (1500-2500 bps). A 50 bps prime hike? Your balance accrues faster—pay down aggressively.

Worked Examples: Basis Points Brought to Life

Theory sticks with stories. Let's crunch numbers.

Mortgage Rate Shift

Your rate climbs from 6.50% to 6.75%. Difference? 0.25%, or 25 bps (6.75 - 6.50 = 0.25; ×100 = 25). On a $400K loan, that's ~$58 extra monthly. Small shift, big bite.

ETF Expense Ratios

An ETF charges 0.03% annually. That's 3 bps (0.03 × 100). Invest $100K? You pay $30/year versus $1,000 at 1% (100 bps). Compounded, it supercharges returns.

These aren't hypotheticals—they're daily decisions shaping wealth.

Your Easy BPS to Percentage Converter: Try It Now

Mastered the math? Supercharge it with our free BPS to percentage converter. Punch in numbers for instant results—perfect for on-the-go investors eyeing Fed dots or yield curves. No sign-ups, just clarity.

"In finance, precision isn't optional—it's your edge."

Next Fed meeting, you'll decode headlines like a pro. Basis points: small unit, massive impact. Dive deeper into rates, yields, and strategies—your portfolio thanks you.